THE AUTOMOTIVE INDUSTRY IN MEXICO

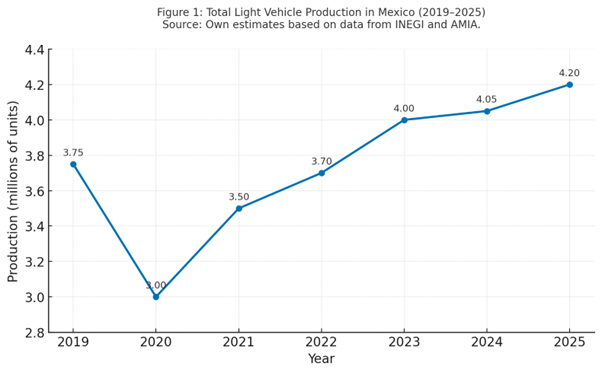

Mexico has established itself as one of the world’s seven automotive powerhouses, producing 4 million light vehicles in 2023 according to the OICA.

1. Quick Overview: Why Mexico Matters

Mexico has established itself as one of the world’s seven automotive powerhouses, producing 4 million light vehicles in 2023 according to the OICA. This performance positions it as Latin America’s top producer and the world’s fourth-largest exporter, with a trade surplus exceeding 99 billion dollars. The sector represents nearly 18% of manufacturing GDP and 32% of national exports, explaining why Mexico’s economy depends so heavily on its evolution.

In 2025, INEGI records showed 2.3 million units manufactured between January and July, a 0.7% increase compared to the previous year and the best historical accumulation for that period. Activity is concentrated in two industrial corridors: the Central-Bajío-Western region, where Honda, Toyota, and Mazda operate, and the Northeast, dominated by General Motors, Stellantis, and KIA. These regions maintain close logistical integration with the United States, ensuring competitiveness, short delivery times, and robust supply chains.

Beyond its economic impact, the automotive sector has a visible social effect. It employs more than 900,000 workers directly and creates around three million indirect jobs, from engineers to logistics providers. Consumers benefit from greater variety and price stability since nine out of every ten vehicles produced are exported tariff-free under the USMCA, preventing cost increases. Each car produced in Mexico embodies innovation, technology, and advanced manufacturing.

The combination of talent, location, and trade agreements makes Mexico an irreplaceable node in the global automotive chain. The resilience demonstrated after the pandemic and the chip crisis shows that the country not only assembles but also sustains the global flow of vehicles. The challenge now is to move from volume to value by incorporating technology development, software, and sustainable manufacturing.

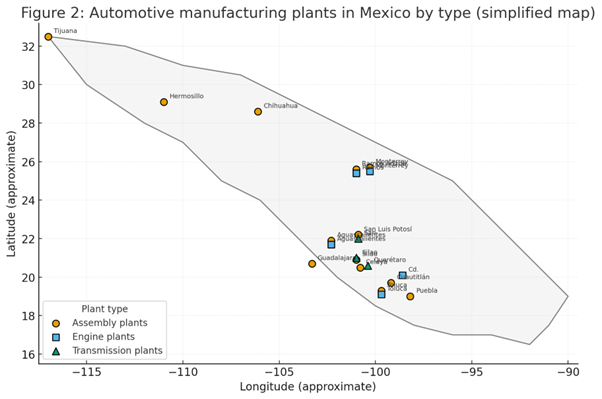

2. Where Cars Are Made

Mexico’s automotive map spans more than 15 states, but its heart beats in the Bajío and the North. Guanajuato leads with four plants: General Motors, Toyota, Honda, and Mazda. Aguascalientes has three Nissan facilities, one shared with Mercedes-Benz. Puebla produces the legendary Jetta and the Q5 SUV for Volkswagen and Audi. In Coahuila, GM and Stellantis operate; in Nuevo León, KIA and Mercedes; while San Luis Potosí hosts BMW and GM. This network illustrates the country’s deep industrial diversification.

Together, national manufacturers boast an installed capacity of more than 5 million vehicles per year, although actual production averages around 4 million. Volkswagen’s Puebla plant, inaugurated in the 1960s, is the largest in the country and one of the brand’s main facilities worldwide, with more than 12 million vehicles produced in its history. In the north, Ramos Arizpe (Coahuila) and Pesquería (Nuevo León) have become export hubs for North America.

Strategic location is crucial. The country is crossed by logistics corridors connecting the Bajío with the ports of Veracruz and Lázaro Cárdenas, as well as the border crossings of Laredo, Pharr, and Nogales. This multimodal network lowers logistics costs and supports a constant export flow. Thanks to it, a vehicle built in Puebla can reach a dealership in Chicago in less than a week, reinforcing Mexico’s comparative advantage over Asian competitors.

Mexico not only assembles cars but also produces engines, transmissions, and electrical systems that supply plants across the region. The interconnection between states generates synergies between OEMs and local suppliers, explaining why the country has become North America’s automotive workshop. This territorial structure provides flexibility amid global shifts and will be the foundation for the transition toward electromobility.

3.What and How Much Is Produced

The production leadership is divided among General Motors (509,000 units), Nissan (389,000), and Ford (242,000) during the first half of 2025. They are followed by Stellantis and Volkswagen, while Toyota and KIA stand out for their accelerated growth of 48% and 11%, respectively. Mexican production is concentrated in light vehicles, mainly SUVs and pickups, which make up three-quarters of the total. In the heavy-vehicle segment, Mexico produced 213,000 units in 2024, the second-best record in history.

The light-vehicle segment dominates because it serves the North American market, where the preference for trucks and SUVs remains strong. Mexican automakers adapt their production mix with models like the Chevrolet Blazer, Toyota Tacoma, and KIA Seltos. Compact cars such as the Nissan Versa and VW Jetta hold a smaller but strategically important share due to their consistent turnover. The domestic market absorbs only about 15% of total production, while the rest is exported.

The technological component of Mexican-made vehicles has grown rapidly. In 2023, nearly 60% of all models included ADAS (Advanced Driver Assistance Systems), intelligent navigation, or wireless connectivity. This forces plants and suppliers to integrate advanced electronics and stricter quality controls. The country is moving toward more sophisticated manufacturing, where engineering and digitalization are as essential as steel.

Looking ahead to 2026–2027, projections place Mexico among the world’s top six producers if new electromobility investments, including Tesla’s plant in Nuevo León, are consolidated. With a stable production base and strengthened rules of origin, growth will depend more on innovation than on the number of assembly lines. The challenge is to maintain efficiency and sustainability without losing competitiveness.

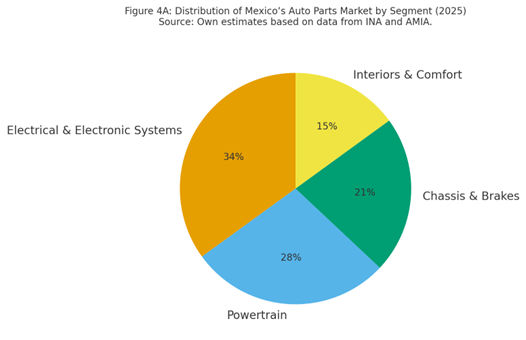

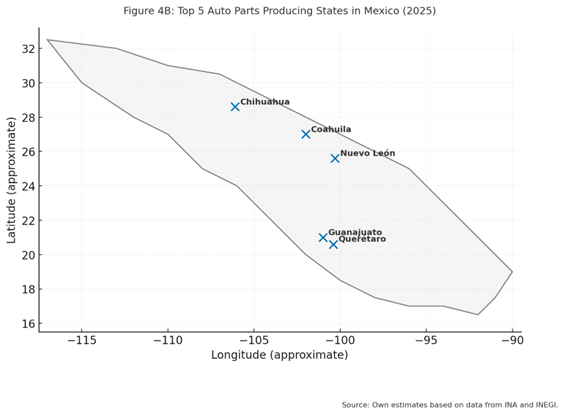

4. Auto Parts: The Other Giant

Mexico’s auto parts industry generates more value than final assembly. In 2023, production reached a record 121.16 billion dollars according to the INA, representing a 16.5% increase. About 87% of this total was exported to the United States and Canada, strengthening North American integration. Mexico is the world’s fourth-largest component producer, specializing in engines, transmissions, electrical harnesses, brakes, seats, and steering systems. This ecosystem supports the country’s 20 assembly plants and hundreds of facilities abroad.

The leading states by value are Coahuila, Guanajuato, Nuevo León, Chihuahua, and Querétaro, which together account for 80% of total output. Each region has its own specialization: Coahuila in powertrain systems, Guanajuato in transmissions, Nuevo León in casting and electronics, Chihuahua in wiring harnesses, and Querétaro in control systems. The nearshoring boom attracted over 2 billion dollars in foreign direct investment in 2023 alone, boosting technological modernization and high-skilled employment.

This growth has structural implications. Mexico has evolved from an assembler to a full supplier within the USMCA bloc, producing essential parts with full traceability. The increase in regional content—from 62.5% to 75%—has driven global companies to relocate production from Asia to northern Mexico. The result is shorter supply chains, lower logistical risk, and more stable consumer prices.

The next step is to move into electronic and sustainable components such as batteries, inverters, and sensors for electric vehicles. Companies like Bosch, Continental, and ZF are already developing advanced modules in Mexican plants. If the country consolidates this transition, it could capture a higher-value technological segment and secure its role as the industrial base of the future.

5. USMCA Made Simple

The United States–Mexico–Canada Agreement (USMCA) defines the framework for automotive integration. For a vehicle to move tariff-free, at least 75% of its core components must originate within the region. This requirement, which replaced the NAFTA threshold of 62.5%, has strengthened Mexico’s industrial base and sparked a wave of relocations. Today, more than 90% of vehicles exported from Mexico meet the rule, ensuring stability for manufacturers and competitive prices for consumers.

Traceability has become a top priority. Every engine, transmission, or electrical system must certify its origin through digital platforms. This has increased transparency and encouraged the use of local suppliers. The immediate result is a more sophisticated value chain, with plants now integrating processes that were once imported. The benefit is not only tariff-related: vehicles produced within the region are also more resilient to global disruptions.

For consumers, the USMCA provides greater price stability and predictability. If the rules were broken, car prices in North America could rise by as much as $2,400 per unit, according to the USITC. Maintaining integration allows vehicles to circulate without added costs and companies to keep investing. Every car produced in Mexico supports thousands of jobs across the border region and ensures the steady flow of auto parts within the bloc.

The next challenge will be the 2026 review, which will assess compliance and potential rule updates. Mexico enters this process well-positioned, having increased regional content and demonstrated adaptability. What is at stake is not just tariffs but the stability of an industrial chain that moves more than $300 billion in trilateral trade each year.

6. From Engine to Chip: The Technological Transition

The modern car is a computer on wheels. Each vehicle now includes more than 1,000 chips on average, three times more than a decade ago. The global trend toward electrification has completely redefined the industry. Mexico already assembles hybrid, plug-in hybrid, and fully electric models such as Ford’s Mustang Mach-E in Cuautitlán and Audi’s Q5 TFSI e in Puebla. These production lines represent the spearhead of the transformation that is underway.

Hybrid vehicles (HEV) combine combustion engines with electric propulsion, while plug-in hybrids (PHEV) can operate solely on stored energy. Fully electric vehicles (BEV) eliminate the traditional engine and rely on high-voltage batteries. For Mexico, manufacturing these models means adapting production processes, training workers, and developing new suppliers for components such as batteries and control systems. The transition is not immediate, but it is advancing steadily.

Beyond electrification, cars are becoming intelligent and connected. ADAS systems, such as automatic braking and lane-keeping assistance, are already standard in 70% of new models. The value of electronics per vehicle will double by 2028, driving demand for automotive software engineers. Mexican plants are implementing flexible production lines capable of alternating between combustion and electric models according to global demand.

For consumers, this revolution translates into greater safety, efficiency, and comfort. A modern vehicle saves fuel, updates itself via the internet, and reduces emissions. In the coming years, consumers will see a growing range of locally manufactured electric models with gradually more affordable prices. The future of the automotive sector no longer depends solely on mechanics but on electronics and the innovation that Mexico can integrate.

Main milestones: From Combustion to Electrification (2000–2030)

- 2000: Optimized combustion engines (efficiency and emission reduction).

- 2005: First commercial hybrids (Toyota Prius, Honda Insight).

- 2010: Expansion of electric vehicles with Nissan Leaf and Tesla Model S.

- 2015: Introduction of ADAS (Advanced Driver Assistance Systems) level 1 and 2.

- 2020: Mass electrification and 4G connectivity, vehicles linked to the digital ecosystem.

- 2025: Transition toward Software-Defined Vehicles (SDV), where software defines performance.

- 2030 (projection): Full integration of AI, 5G networks, and advanced autonomy.

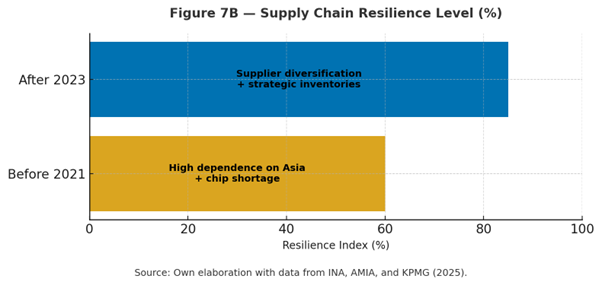

7. Semiconductors and Supply Chain

The 2021 microchip crisis exposed the fragility of global supply chains. When Asian factories halted production, Mexican carmakers were forced to suspend shifts due to component shortages. In some cases, vehicles were delivered without electronic functions or with long delays. The problem stemmed from the fact that automotive chips rely on mature technologies, which are less profitable for manufacturers that prioritize sectors like smartphones and computers.

The industry responded with a new resilience strategy. Companies now maintain safety inventories, certify secondary suppliers, and sign direct agreements with semiconductor manufacturers. Firms such as Rochester Electronics and NXP are collaborating to produce “legacy” chips that guarantee continuity. This shift requires long-term planning and early detection of obsolescence, reducing the risk of production stoppages on assembly lines.

The impact on consumers was clear. In 2022, waiting times for new cars exceeded six months. By 2024, they had dropped to one or two months. Today, Mexican supply chains operate with much greater stability. The key lesson is simple: local integration of electronic components is essential to maintaining competitiveness. Mexico is already exploring projects for semiconductor technology parks in Nuevo León and Jalisco with support from the government and private sector.

Control over technological supply is the new industrial “oil.” The pandemic experience accelerated a regional policy to reduce dependence on Asia. In this context, Mexico has the opportunity to position itself as a manufacturing hub for automotive chips, leveraging its location and close partnership with the United States, which promotes its own CHIPS Act. If successful, the country will not only assemble vehicles but also produce their electronic brains.

8. Talent, Education, and Clusters

The new automotive profile is hybrid, combining expertise in mechanics, electronics, and software. Companies are looking for “system orchestrators,” professionals capable of integrating sensors, engines, and code into a single product. Universities and manufacturers are working together on dual programs and certifications in electromobility, mechatronics, and automotive software development. Technical education is becoming a key regional competitive advantage.

Events such as the Business Automotive Meeting (BAM), the International Automotive Industry Congress (CIIAM), and the Automotive Talent World Summit (ATWS) serve as forums where academia, government, and the private sector align efforts. They discuss innovation, digitalization, and workforce development strategies. These platforms strengthen collaboration among state clusters and promote technology transfer.

Automotive clusters in Guanajuato, Nuevo León, Querétaro, and Coahuila act as coordination networks. They bring together OEMs, suppliers, and universities to address common needs such as SME certification, workforce training, investment attraction, and R&D development. According to the National Network of Automotive Clusters, these alliances have created more than 900 local suppliers and thousands of technical jobs, driving industrial decentralization.

The future of Mexico’s automotive talent depends on adaptability. As cars integrate more software, the country will need engineers who can “speak the language of algorithms.” If universities align closely with industry needs, Mexico will be able to offer not only manufacturing but also innovation. The key will not just be to produce vehicles but to design the solutions that power them.

9. Outlook for 2026–2027

By 2027, Mexico faces three possible scenarios. The baseline projects stable production of 4.2 million vehicles with full compliance with the USMCA and moderate growth in auto parts. The optimistic scenario forecasts more than 5 million units, driven by new investments, higher regional content, and the launch of Tesla’s plant in Nuevo León, which would make Mexico the world’s sixth-largest vehicle producer. The challenging scenario anticipates a slowdown if the U.S. economy cools down, if the USMCA review introduces new restrictions, or if energy shortages persist in some industrial regions.

Opportunities are clear. The rise of nearshoring and electrification has drawn attention from Asia and Europe. The challenge will be transforming volume into value through local engineering, automation, clean energy, and a more sophisticated supply network. States such as Guanajuato, Nuevo León, Querétaro, and Coahuila are emerging as natural leaders in this new industrial phase, as long as they continue investing in infrastructure, technical education, and talent development.

For consumers, the coming years will bring a more diverse and technologically advanced vehicle offering. Local automakers will expand their range of hybrid and electric models, while improvements in logistics and chip availability will shorten delivery times. Prices may stabilize if inflation remains under control and regional integration keeps input costs contained. Mexican consumers will enjoy greater innovation and access to sustainable models made within the country.

The 2026–2027 horizon will mark a turning point. If Mexico consolidates its technological capacity and strengthens its value chain, it will move from being North America’s assembly workshop to becoming its center of industrial innovation. The key will not be to produce more, but to produce better: cleaner, smarter, and safer vehicles that reflect the evolution of an industry that no longer just assembles but designs the future of regional mobility.

mantente al día con DICEX