TRANSPORTATION COSTS IN MEXICO 2025: HIGHWAY VS. RAILWAY

With the rise of nearshoring and the expansion of manufacturing, the cost of moving goods within the country has become a strategic issue.

Mexico is at a decisive moment for its logistical competitiveness. With the rise of nearshoring and the expansion of manufacturing, the cost of moving goods within the country has become a strategic issue. Ground transport, which carries the vast majority of shipments, is facing inflationary pressures from fuel, tolls, and maintenance, while rail transport seeks to gain ground as a cheaper alternative, though still limited by coverage and transit times.

2025 Outlook: The Cost of Moving Freight in Mexico

In 2025, transporting goods across Mexico has become more expensive than in previous years. The beginning of the year was marked by a 6.7% increase in freight transport rates, the steepest jump since 2023. This rise is largely explained by higher prices of strategic inputs, particularly fuel. Diesel, which accounts for roughly one third of a carrier’s operating costs, rose 16.7% year over year in January and reached 26 pesos per liter by September. The result was a higher cost per kilometer and tighter profit margins.

These adjustments were not limited to fuel. During the same period, lubricant prices rose around 6%, new freight vehicles increased by roughly 8%, and spare parts by 7.5%. Tire prices went up 4.5%, and specialized trailer accessories nearly 7%. At the same time, toll rates increased by an average of 6.5% after Caminos y Puentes Federales (CAPUFE) applied hikes of 5% to 7% on key highways such as Mexico–Querétaro and Monterrey–Nuevo Laredo. These increases significantly raised the cost of each trip. On long routes, tolls can represent up to one fifth of total operating expenses.

The National Producer Price Index (INPP) confirmed this trend. Road freight transport rose more than 3.8% annually in July 2025, while toll and lubricant services increased above overall inflation. In aggregate, freight companies saw their revenues grow 7% annually between January and May, but operating expenses climbed 7.9%. Margins narrowed and it became harder to pass rising costs to end customers.

Even so, this dynamic did not cause a sharp contraction in activity. The manufacturing boom and nearshoring kept shipment volumes steady, especially in automotive and electronics. These industries depend on a constant flow of parts and equipment across the northern border. However, a slight slowdown appeared midyear. In April and May, real trucking revenues dropped around 1.5% year over year, partly due to lower demand linked to U.S. tariffs and the inability to fully absorb cost increases.

From a competitiveness standpoint, 2025 presents a dual challenge. Companies face higher costs in fuel, inputs, and security, which drives up domestic transport and export prices. At the same time, the opportunity to consolidate Mexico as a strategic nearshoring hub requires balancing these increases with efficiency, technology, and greater integration of alternative modes, particularly rail, which offers advantages in scale and per ton costs. This year makes it clear that transporting goods in Mexico is more expensive than in 2024, but it also shows that rising supply chain pressures are pushing companies to rethink how and where they move their freight

Road Freight Under Cost Pressure

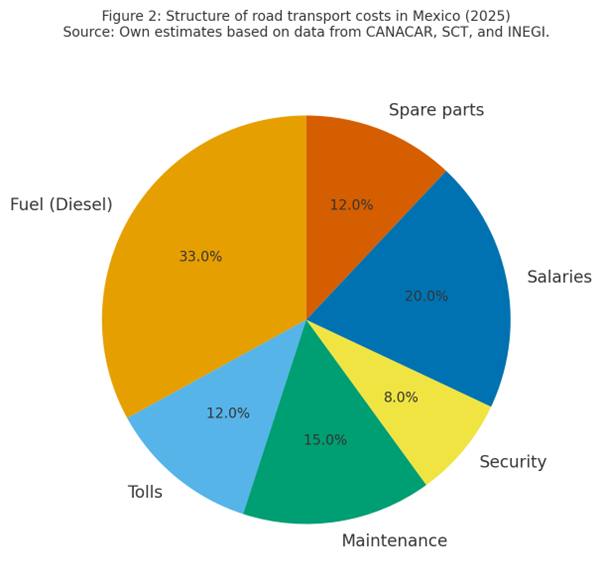

In 2025, trucking remains the backbone of freight movement in Mexico, responsible for more than 56% of all ground shipments. Its importance is undeniable in industries such as automotive and export manufacturing, which rely on the flexibility and reach that trucks provide compared with rail. However, this central role also makes it more vulnerable to cost shocks. Fuel, tolls, wages, and parts have all risen steadily over the past 18 months.

Diesel, which accounts for roughly 33% of fleet operating costs, climbed nearly 7% between January 2024 and September 2025. The national average price rose from 24.41 to 25.85 pesos per liter. On long northern routes such as Monterrey–Nuevo Laredo or Monterrey–Saltillo, fuel can represent up to 40% of total logistics expenses. This has forced carriers to apply surcharges of 8% to 12% during 2025. Toll hikes, an average of 7% implemented by CAPUFE in January, have also directly impacted long haul routes.

Driver wages have risen as well due to a shortage of qualified labor. The average monthly salary for fifth wheel tractor trailer operators in northern Mexico is about 23,000 pesos, with performance bonuses pushing it up to 30,000. This labor pressure translates into a 5% to 6% increase in the wage component of cost structures. Preventive maintenance, lubricants, and spare parts have also risen sharply. The INPP reported an 8.3% annual increase in July 2025 for the auto parts category.

The result is a challenging outlook. According to the National Chamber of Freight Transport (CANACAR), the average cost per kilometer traveled by truck rose from 18.5 pesos in 2024 to 20.1 pesos in 2025, an 8.6% increase in just one year. This has led to visible rate hikes in domestic freight, pressuring key industries to renegotiate contracts and adjust margins.

More specifically, data from the Ministry of Infrastructure, Communications, and Transport (SICT) show that a typical Monterrey–Mexico City trip in an articulated truck rose from an average of 48,000 pesos in 2024 to 52,500 pesos in September 2025, a 9.3% jump. Fuel costs account for nearly 19,000 pesos of that total, while tolls exceed 7,200 pesos. These figures explain why many carriers have shifted part of their fleets to double trailer operations. Although they require stricter safety compliance, they reduce per ton costs by roughly 12%. Cost pressure is not uniform. On export routes toward the border, increases hover around 10%. On internal Bajío routes, rises are closer to 6%.

Rail: Competitiveness and Cost per Ton Kilometer

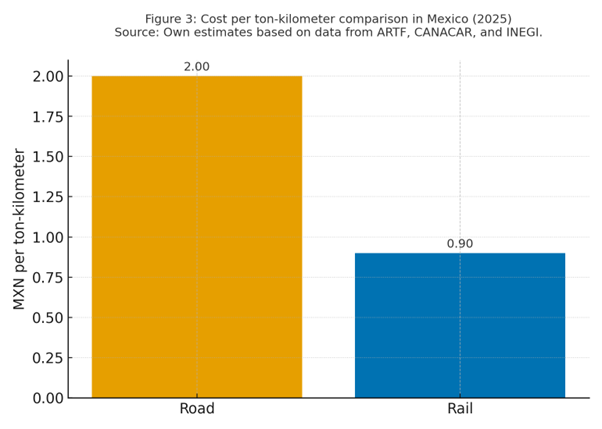

Rail transport has gained relevance as a more cost competitive alternative to trucking. In 2025, moving cargo by train is up to 38% cheaper per ton kilometer than by road. This savings comes from economies of scale. A 100 car train can replace roughly 280 trucks, which drastically reduces spending on fuel and operators. Rail carried over 132 million tons in 2024, equal to 19% of all ground freight, and it continues to grow in 2025 thanks to key sectors such as automotive, mining, and agriculture.

Rail costs have remained more stable than highway costs. Although diesel prices also affect locomotives, fuel consumption per ton moved is far lower. As a result, rail tariffs have risen only 3% to 4% annually, below the trucking average. However, limited infrastructure and reliance on private concessions remain major bottlenecks that hold back the sector’s growth.

Another key factor is international connectivity. Rail’s strength lies in northern industrial corridors that link Monterrey, Saltillo, and the Bajío with the U.S. border. These routes are essential for the automotive industry, which depends on a steady flow of parts and vehicles to plants in Texas, Michigan, and other states. Coverage toward southern Mexico remains weak, which limits the rail network’s reach into agricultural and energy sectors.

The challenge for rail in 2025 is to solidify competitiveness without losing reliability. Congested tracks, community blockades, and customs delays still affect efficiency. Even so, outlooks indicate that rail could become the fastest growing transport mode over the next decade if investments in infrastructure and intermodal logistics continue to expand.

Road vs. Rail: The Battle of Time

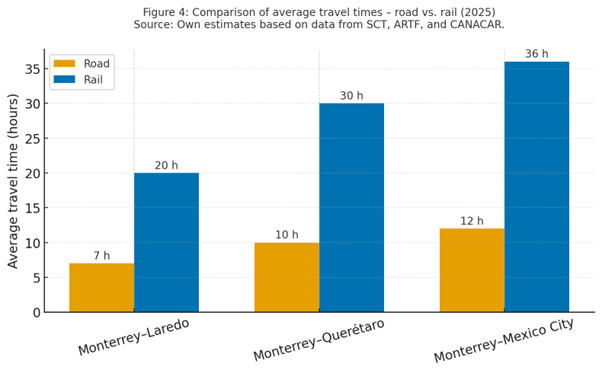

Cost is not the only factor that defines competitiveness. Time is just as critical. In 2025, road transport retains an advantage in speed and flexibility, while rail offers lower rates but longer transit times. Moving cargo from Monterrey to Laredo by truck takes 6 to 8 hours on average, compared with 18 to 24 hours by train, depending on border crossings and rail availability.

On domestic routes, trucks also maintain the edge in immediacy. For example, a Monterrey–Querétaro trip by road takes about 9 to 10 hours, while by train the same route can take up to 36 hours due to lower service frequency and longer loading and unloading processes. These differences explain why, despite lower rail costs, many industries still favor trucking when just in time deliveries are required.

However, the gap has narrowed in some strategic corridors. In 2025, modernization of rail crossings in Nuevo León and Coahuila has shortened border dispatch times, cutting up to six hours on certain shipments to the United States. In addition, digital customs systems and more efficient cargo management have improved rail reliability.

The trade off between cost and time will remain central to Mexican logistics. For high value goods such as electronic components or critical auto parts, road transport will remain the first choice. For raw materials or lower urgency goods, rail provides clear cost advantages even with longer transit times.

According to the Rail Transport Regulatory Agency (ARTF), average rail transit times in 2025 are 150% to 200% longer than trucking on main routes. This means that while a truck completes a Monterrey–Mexico City trip in about 12 hours, a train may take up to 36, plus 4 to 6 hours of yard delays. Still, improvements at crossings such as Piedras Negras and Nuevo Laredo already show reductions of up to 15% in rail waiting times. If modernization continues at this pace, rail could close the gap in the next decade and become a more viable option not only in cost but also in reliability.

Security: The Hidden Cost of Transport

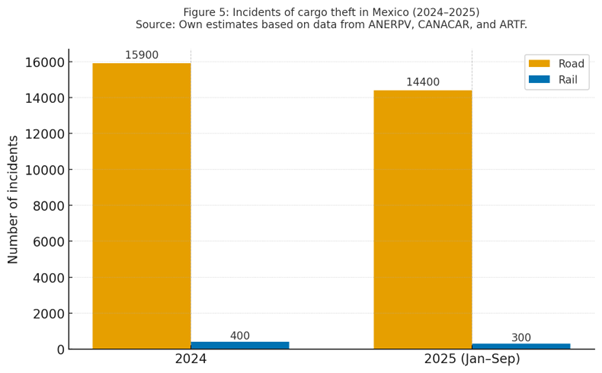

Insecurity has become one of the most expensive factors affecting transport in Mexico. In 2025, reports of cargo theft remain high, averaging 1,200 incidents per month according to CANACAR. More than 15,900 events were recorded in 2024, and by the first nine months of 2025 more than 14,000 had already occurred, which shows that the problem persists. The states most affected are Puebla, State of Mexico, and Guanajuato. Northern corridors such as Nuevo León and Tamaulipas are not exempt.

The economic impact is both direct and multifaceted. Each theft entails losses of 350,000 to 500,000 pesos in goods, in addition to higher insurance premiums, escort expenses, and extra stops to ensure driver safety. These factors raise operating costs and cause supply chain disruptions that affect both manufacturers and distributors. Security related expenses can account for 7% to 10% of total trip costs in high risk zones.

By contrast, rail shows much lower incidence. According to ARTF, around 400 theft or vandalism incidents were reported on trains in 2024, and fewer than 300 cases by September 2025. The most problematic stretches are in Veracruz, Puebla, and Guanajuato, typically linked to community blockades or illegal cargo siphoning. This difference has made rail a safer option for high value goods, although limited coverage prevents it from absorbing greater demand.

Business perception confirms the gap. Seven out of ten trucking companies consider insecurity the main threat to their operations in 2025, while the rail sector views it more as an operational challenge than a structural risk.

Insecurity not only raises operating costs. It also reshapes how supply chains are planned. Many companies have shifted to daytime transits, added specialized insurance, and hired security escorts, which means longer delivery times and greater logistical complexity. This phenomenon increases road transport costs by at least 7% on high risk corridors and underscores the need to strengthen security on federal highways to sustain Mexico’s logistics competitiveness.

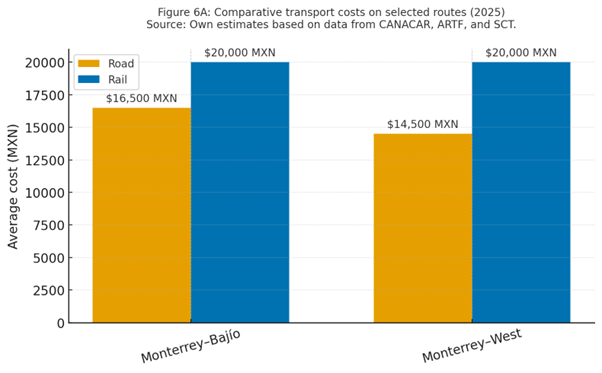

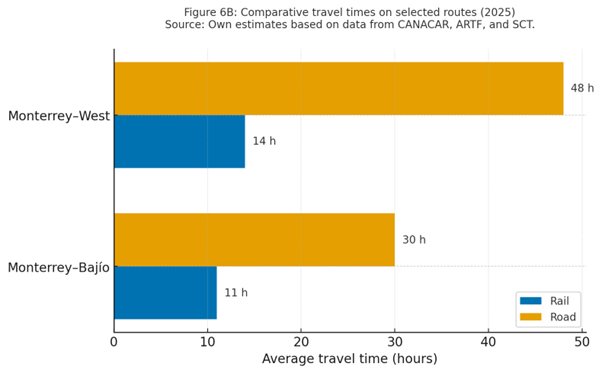

Comparative Case: Monterrey–Bajío and Monterrey–West Corridors

Northern routes connecting to central and western Mexico provide a clear picture of current logistics costs. The Monterrey–Bajío corridor, vital for the automotive industry, shows an average cost of 45,000 pesos per truck trip in September 2025, an 18% increase from the same month in 2024. This rise is mainly due to higher tolls on highways such as San Luis Potosí–Querétaro and León–Celaya, along with diesel hikes. Travel time remains 9 to 10 hours, although security risks in parts of Guanajuato have forced some companies to add escorts.

The Monterrey–West route, which connects to Guadalajara and Colima, shows a different pattern. The average cost there is 58,000 pesos per trip, up 15% year over year, slightly less than the Bajío route. The main reason is fewer toll booths along the way, although the total distance is longer and transit times reach 14 to 16 hours. For automotive and electronics companies supplying the El Salto industrial corridor in Jalisco, this route is critical, but it is more vulnerable to delays from highway blockades in Michoacán.

Rail on both routes offers significant savings, although with much longer transit times. For Monterrey–Bajío, moving goods by train can be up to 25% cheaper, but it takes 30 to 36 hours. For Monterrey–West, savings reach up to 28%, with shipment costs around 14,500 pesos, though delivery times exceed 48 hours. These differences explain why many companies adopt mixed strategies. They use trucks for critical parts and trains for raw materials or non urgent freight.

These routes highlight the core dilemma in Mexican logistics. Companies can pay more for speed and flexibility, or they can sacrifice time to cut costs. The decision depends on the sector and cargo value. In both cases, cost pressure is clear and forces companies to rethink distribution strategies.

Economically, these routes carry great weight. The Monterrey–Bajío corridor moves more than 6 million tons per year, while Monterrey–West exceeds 4 million. The 20% cost difference between road and rail can translate into multimillion peso savings for companies that plan ahead. However, the longer rail times require maintaining inventories equivalent to two or three days of production, which raises financial costs. This duality confirms that Mexico’s transport future will rely on hybrid solutions in which rail delivers efficiency and trucking ensures speed.

From Cost to Efficiency: Facing the Cost Storm

Rising transport costs in 2025 have forced companies to rethink their logistics models. Higher prices in fuel, tolls, and wages directly affect freight rates, which makes the search for efficiencies a top priority. One widespread strategy is route optimization through digital systems that reduce kilometers traveled and maximize return loads. Such measures have achieved cost reductions of up to 8% in some fleets.

Faced with escalating expenses, logistics and transport companies have turned to more aggressive tactics. Load consolidation, which optimizes every trip and minimizes empty runs, has become common practice. Meanwhile, the use of full trailers, or double units, is expanding on long northern routes. This allows up to 40% more volume with only marginal increases in fuel consumption. These practices are now essential for automotive and manufacturing sectors, where moving large volumes at lower cost is key to competitiveness.

Fleet renewal with more fuel efficient units also plays a central role. Although it requires high upfront investment, the medium term savings are considerable. A Euro VI tractor consumes up to 12% less diesel than older models. Interest is also growing in alternative fuels such as compressed natural gas and biodiesel. At the same time, some operators are experimenting with hybrid and electric trucks. Their share is still small, but it is expected to accelerate by 2026 with supportive policies and financing.

Digital technology has become a strategic ally. Fleet management platforms, telemetry, and real time monitoring enable tighter control of operator performance and preventive maintenance. These tools reduce downtime, optimize load efficiency, and enhance security, which lowers costs and improves reliability. In addition, driver training in fuel efficient driving techniques can cut consumption by 5% to 7%.

Rail is also emerging as a key element in strategies to contain costs. Intermodal partnerships that combine truck and rail allow a better balance between time and price. On certain corridors, they can cut expenses by up to 15%. The key lies in improved coordination between carriers, rail concessionaires, and clients, supported by investment in intermodal terminals and transfer yards.

Finally, logistics planning has become a decisive factor. Companies that anticipate shipments, schedule efficiently, and align inventories with seasonal demand can achieve significant savings. In an environment where transport is increasingly expensive and risky, the ability to plan and adapt will define competitiveness in the years ahead.

Containing rising costs does not depend on a single measure. It requires a combination of operational efficiency, technological innovation, and multimodal integration. Load consolidation, double trailers, digitalization, fleet renewal, and intermodality are becoming the pillars of a more resilient logistics model. These actions mitigate current cost pressures and prepare the sector for a future in which Mexico’s competitiveness will hinge on balancing cost, time, and security across logistics.

mantente al día con DICEX