MEXICO'S FOREIGN TRADE IN 2025: A COMPLETE OVERVIEW

In 2025, Mexico's foreign trade is showing favorable results, with a trade surplus of 1.416 million dollars in the first seven months of the year.

A Manufacture-Driven Surplus

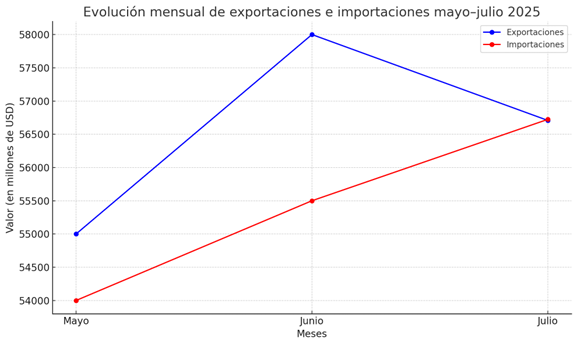

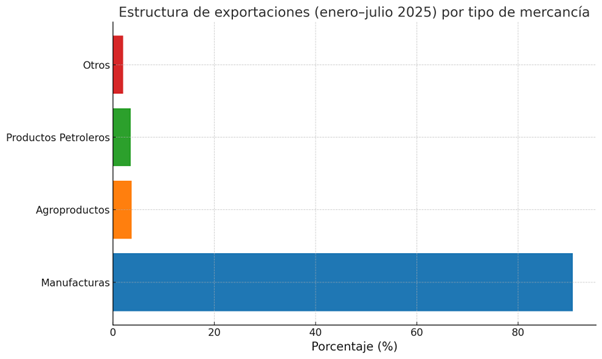

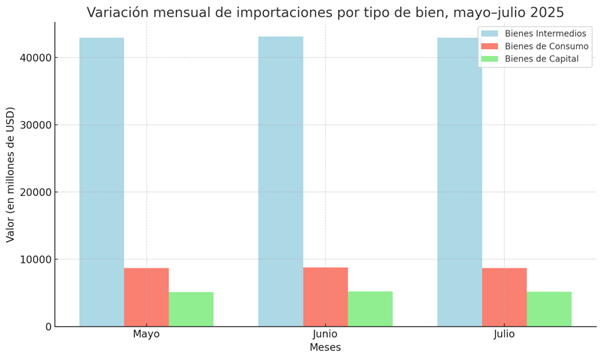

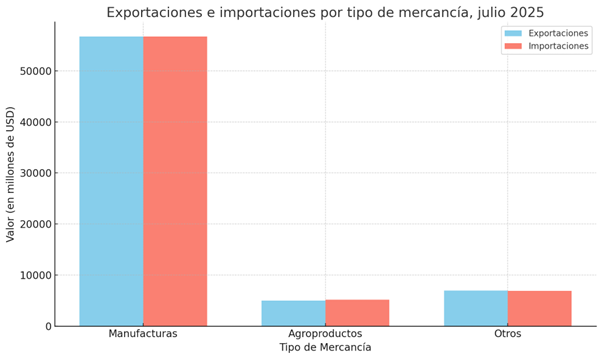

For the first seven months of 2025, Mexico achieved a trade surplus of 1.416 million dollars (MDD). In this period, exports totaled 369.436 mdd, while imports reached 368.020 mdd, according to the most recent data from INEGI. In July alone, exports grew 4.0% annually to 56.708 mdd, and imports rose 1.7%, with a total of 56.724 mdd. This uptick in exports is particularly relevant, as manufacturing continues to be the engine of the country's foreign trade, representing 90.8% of total exports. The United States remains the top destination, absorbing 84.03% of non-oil sales. In the case of imports, intermediate goods accounted for 76.8% of the total, followed by consumer goods (14.4%) and capital goods (8.8%). In the customs area, ANAM revenue reached a historic level of 711.9 billion pesos in the first half of 2025, reflecting the growing weight of key customs offices such as Nuevo Laredo and Manzanillo.

This surplus marks an important change compared to previous years, when Mexico had been recording significant deficits. The result reflects greater export competitiveness, especially in manufacturing, agricultural and electronic products. Sales to the United States grew moderately, while imports of intermediate and consumer goods remain the most important, with a strong dependence on inputs from the United States and China. At the same time, customs collection reached record numbers, reflecting the strengthening of logistics infrastructure and international trade.

Exports and Imports

In 2025, Mexico's foreign trade is showing favorable results, with a trade surplus of 1.416 million dollars in the first seven months of the year. This contrasts with the deficit of -10.916 mdd recorded in the same period in 2024. The change reflects a significant boost in exports, especially in the manufacturing sector, together with a moderate and more controlled growth in imports compared to previous years.

During the first half of 2025, Mexico exported 369.436 mdd, which represented a year-on-year increase of 4.3% compared to the same period in 2024. This performance confirms the strength of manufacturing as the main driver of foreign sales. At the same time, imports totaled 368.020 mdd, with an increase of just 0.5%, reflecting some stagnation in foreign purchases and which, in turn, favored the positive trade balance.

In July 2025, exports and imports performed more evenly: exports grew 4.0% and imports 1.7%. Although the increase in imports was lower, intermediate and consumer goods maintained their predominance, highlighting the rise in technological products and machinery. This confirms that the Mexican industry is increasingly integrated into global production chains.

Exports: The Sectors That Drive Growth

Mexican exports continue to be dominated by the manufacturing sector, which represents 90.8% of the total, with solid growth in key areas such as electronics, industrial machinery and auto parts. It should be noted that, in July 2025, exports of machinery and equipment increased 28.7% per year, reflecting the recovery of the domestic industry and its growing competitiveness on the international stage. The 10.2% increase in exports of electronic equipment also stood out, confirming Mexico's position as a producer of technological goods with high added value.

Within the manufacturing sector, the automotive industry remains a crucial sector. Although automotive exports fell 7.0% in July 2025, mainly due to a drop in sales to the United States (its most important market), the growth in exports of auto parts and cargo vehicles to other destinations shows a process of diversification. That same month, Mexican exports to Europe (especially Germany and Spain) grew 12.0% year-on-year, evidencing a greater insertion in markets outside North America.

The agricultural sector, although with a lower weight in exports (3.7%), has also shown good performance. Products such as avocado (+13.7%) and raw coffee (+91.8%) registered strong increases, reaffirming Mexico as a key exporter of high-value agricultural products, especially to the United States. In contrast, traditional goods such as vegetables and tomatoes reported declines, reflecting the challenges faced by agribusiness due to climatic factors and the volatility of global demand.

In the energy sector, oil continues to play an important role in the export basket, although in 2025 oil exports fell 24.8% due to the fall in crude oil prices. Even so, non-oil exports maintain the lead, with manufacturing as the main engine of foreign trade.

Regarding imports, Mexico continues to rely on strategic inputs such as semiconductors, auto parts and electronic products to sustain domestic production. In 2025, semiconductor imports from the United States and China increased, reflecting the strength of the local technology sector, which requires these inputs to produce electronic and telecommunications goods. Auto parts also remain essential imports, as the country depends on specialized components from international markets to assemble and export vehicles globally.

Imports: The Role of Key Inputs and Products

In 2025, Mexican imports maintained moderate and constant growth, reflecting the country's need to acquire strategic inputs to sustain domestic production and consumption. Intermediate goods are still the most relevant, accounting for 76.8% of the total imported goods. This confirms that the Mexican industry is heavily dependent on external inputs, especially in sectors such as the automotive, electronic and chemical industries. Among the most prominent products are auto parts and electronics, mainly from the United States and China. These goods are essential for assembly and production, reinforcing Mexico's role as a global supplier of vehicles and electronic products.

In July 2025, imports of intermediate goods totaled 42.943 mdd, implying a year-on-year increase of 2.5%. This uptick is linked to the increased demand for industrial inputs in key sectors such as automotive and electronics, particularly semiconductors and automotive components, essential for manufacturing high-value products and advanced technology. Although most of these inputs come from the United States, China maintains a prominent role as a supplier of technological and electronic components.

As for consumer goods, imports grew by just 0.4% compared to the previous year, reflecting stable demand but with less dynamism than other sectors. Technological products (such as smartphones, computers and appliances) stand out as the most purchased in this category, driven by the growing interest of consumers in advanced technology. However, purchases of luxury goods and non-essential products have remained limited due to more prudent household spending.

Finally, imports of capital goods fell 2.2% compared to 2024, reaching 5.101 mdd in July 2025. This decline is due to the lack of investment expansion in some industrial sectors, affected by global economic uncertainty. Although Mexican companies continue to require high-tech machinery and equipment to improve productivity, the lack of fiscal incentives and international volatility have held back investment decisions in new technologies and advanced equipment.

Mexico's Top Business Partners: Who Are We Doing Business With?

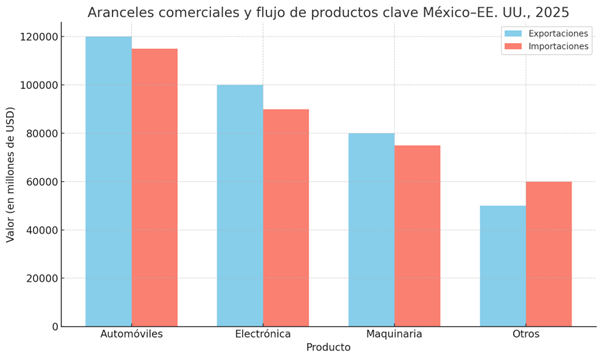

The relationship with the United States continues to be essential for Mexico's foreign trade and, in 2025, it consolidates itself as its main partner, with more than 80% of Mexican exports going to that country. In 2023, exports to the U.S. In the United States, they reached 476.6 billion dollars, representing a year-on-year growth of 4.8%. These figures confirm the importance of the bilateral relationship and the role of the Mexican industry, especially in the automotive, electronic and agro-industrial sectors.

Trade with the United States remains the engine of the Mexican economy, although it also shows vulnerabilities. Exports of cars and auto parts continue to play an important role, but this sector has suffered from the drop in sales to the US market due to tariff tensions and lower demand in some areas. Despite this, advanced technology products and agro-industrial goods remain important sources of export.

Canada is in second place as a trading partner of Mexico within the framework of the T-MEC. Although the volume of trade does not compare with that of the United States, it remains a key ally in agricultural, automotive and manufacturing trade. In 2025, Mexico continues to be the main Canadian supplier of goods such as cars, processed foods and electronic products.

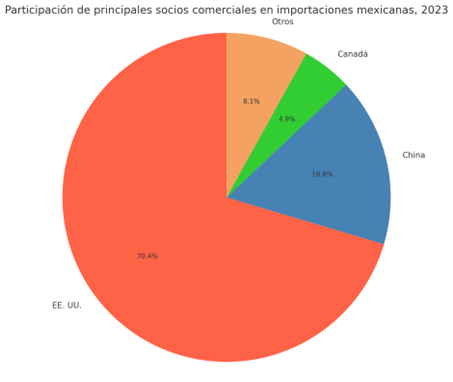

With regard to China, trade presents a challenge. Mexico maintains a trade deficit with this country, since imports of electronic products and auto parts from the Asian giant increased in 2025, evidencing Mexico's dependence on technological goods. This trade relationship, although necessary, generates a significant deficit and underlines the importance of reducing dependence on Chinese inputs. In 2024, imports from China represented 21% of Mexico's total foreign purchases, reflecting the strategic importance of this relationship, especially in sectors such as electronics and industrial inputs.

Mexico's Most Exported and Imported Merchandise

Mexico's exports continue to be dominated by manufactured products, with a strong presence in sectors such as the automotive industry, electronics and machinery. The Mexican automotive industry, in particular, remains a fundamental pillar for the country's exports, with vehicles and auto parts representing a large part of foreign trade. Car exports to the United States continue to be key to the Mexican economy, and are expected to continue to grow in the coming years, although with some occasional setbacks due to trade tensions. In 2025, Mexico mainly exported the following products:

● 8471 — Computers and automatic machines for data processing.

● 8703 — Cars for transporting people.

● 8708 — Parts and accessories for motor vehicles.

● 8704 — Vehicles for transporting goods (trucks/pickups).

● 8517 — Telephones and communication devices.

● 8544 — Electrical conductors (cables).

These products reflect the strength of the Mexican industry in high-tech and advanced manufacturing sectors, allowing Mexico to compete globally in key sectors. Exports of semiconductors, auto parts and electronic products remain essential for value chains in North America and in international markets, and Mexico is consolidating itself as a key player in the electronics industry.

On the other hand, imports from Mexico continue to reflect the need for intermediate goods and technological products to supply Mexican factories and assemblers. Electronic products, such as semiconductors and integrated circuits, remain one of the main import categories, especially from China and the United States. In addition, imports of auto parts remain a key import, since Mexico assembles and exports vehicles globally, and depends on specialized inputs from international markets.

Oil imports are also still essential for Mexico, although in 2025 there has been a reduction in fuel imports due to increased domestic production. In particular, refined petroleum remains the most important import in terms of value, since Mexico still depends on imported fuels to meet its domestic demand. Despite efforts to improve energy self-sufficiency, Mexico remains vulnerable to international oil prices and global market volatility.

Key Customs and the Impact on Mexico's International Trade

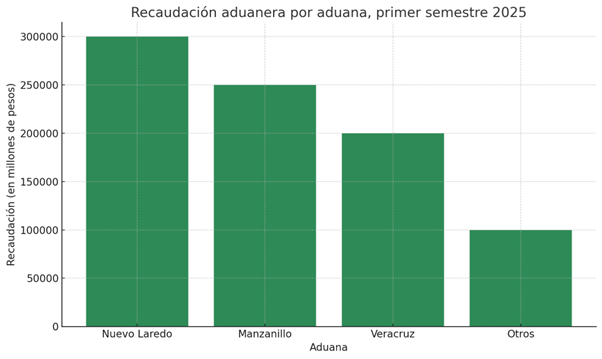

The Mexican customs system continues to play a crucial role in the country's foreign trade, being responsible for managing more than 700 billion pesos in customs collection in the first half of 2025 alone. The most important customs offices continue to be Nuevo Laredo, Manzanillo and Veracruz, which handle the vast majority of goods that cross Mexico's land and sea borders. Nuevo Laredo, in particular, remains the main land crossing for goods, managing 40% of the imports and exports that transit between Mexico and the United States. UU.. Its strategic location along the I-35 corridor, which directly connects Mexico with Texas, makes it a vital logistics hub for trade between the two countries.

Historic revenue in Nuevo Laredo has been driven mainly by automotive, electronic and agro-industrial products, which constitute an important part of the trade between the two countries. This success is also due to investments in infrastructure and the implementation of automation technologies that have allowed a more agile and efficient handling of goods. In addition, the implementation of more transparent and faster customs procedures has improved Mexico's competitiveness at border crossings, favoring Mexican companies that rely on these customs for the export of products to the United States.

As for Manzanillo, it is Mexico's main seaport for trade with Asia and other regions of the world. In 2025, Manzanillo continues to consolidate itself as one of the most active ports in terms of commercial transactions, especially for the trade of electronic products, industrial machinery and agro-industrial products. The increase in exports of avocados and other agricultural products has also had a major impact on the port of Manzanillo, making it a key route for access to international markets.

The port of Veracruz, in the Gulf of Mexico, also remains essential for international trade, especially for the export of energy products and agricultural products. The reconstruction and modernization of the port infrastructure have allowed Veracruz to remain a main gateway for products exported to Europe and Asia. In addition, efforts to strengthen logistics corridors between these ports and the industrial zones of central and southern Mexico are boosting interregional trade, increasing Mexico's competitiveness in global markets.

Regarding customs collection, the National Customs System (ANAM) continues to report record figures, with a collection of 711.9 billion pesos in the first half of 2025, an increase of 23.4% in real terms compared to the same period in 2024. This growth is due to the optimization of customs processes and the adoption of new technologies that allow better management of goods at the border crossing. VAT collection, which represents 70.1% of the total, remains the main source of income, followed by the IEPS and the IGI.

Prices and exchange rate

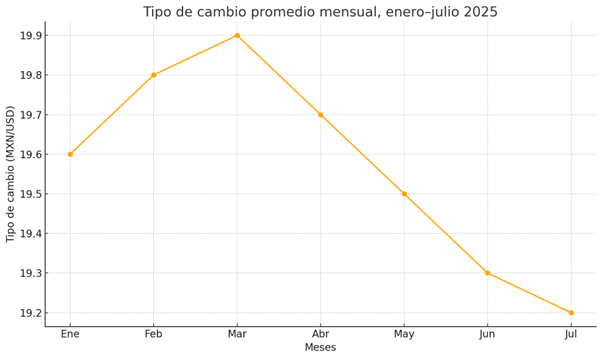

The price environment in Mexican foreign trade showed moderate variations in 2025. In particular, export prices have stabilized compared to the previous year, which has benefited manufacturing sectors and electronic products. However, exchange rate volatility remains a key factor for companies that rely on imports of intermediate goods. The Mexican peso appreciated slightly against the U.S. dollar during the first half of 2025, which has had a positive impact on the competitiveness of Mexican exports, as it has reduced the cost of imported inputs for domestic production.

Despite this appreciation, the peso continues to experience significant fluctuations, especially due to external factors, such as the monetary policy of the U.S. Federal Reserve. Department of State and trade tensions between the United States and other global economies. Mexican exports have benefited from a stronger currency, allowing products manufactured in Mexico to be more attractive to international markets, especially in sectors such as cars and electronics. However, an excessive increase in the value of the peso could have the opposite effect, raising the prices of Mexican products in key markets and affecting export competitiveness.

Imports have also been affected by this appreciation of the peso, as imported intermediate goods have become “cheaper”, especially those that come from the United States. Imports of machinery and electronics have registered an increase in terms of volume, reflecting that Mexico continues to need these inputs for its domestic production. However, the energy sector continues to face difficulties, as Mexico continues to depend on fuel imports, which has generated a deficit in oil imports, which fell by 8.5% in 2025.

Trade Policy Environment

The international trade environment for Mexico in 2025 has been marked by tariff tensions between the United States and China, which has indirectly affected Mexico, given that both countries are key trading partners for the country. The trade war between these two economies has prompted Mexico to take advantage of the nearshoring phenomenon, relocating production from suppliers that previously supplied China to Mexico. This phenomenon has been an indirect benefit for the Mexican economy, as investment has increased in sectors such as automotive and electronics.

However, the protectionist measures adopted by the U.S. The U.S. continues to pose a risk to Mexican exports. In particular, the tariffs applied to steel and aluminum have affected several Mexican companies that rely on these materials for their production. Although the T-MEC remains a fundamental agreement for North American trilateral trade, changes to the rules on tariffs could create additional tensions. In addition, the recent tariff escalation on products such as copper and aluminum has affected the flow of certain key products from Mexico to the United States.

Despite these challenges, Mexico remains a strategic partner for the U.S. Not only because of its geographical proximity, but also because of its ability to offer competitive products in sectors such as automotive, electronics and machinery. In addition, bilateral relations remain strong, as the commercial interests of both countries are highly interconnected, and the growing Mexican industry plays a key role in the U.S. supply chain. UU.

The Future of Mexican Foreign Trade

Mexico's performance in foreign trade during 2025 has been a success story, with a trade surplus achieved thanks to the growth of manufacturing exports and the recovery of key sectors such as automotive and electronics. However, the high concentration in the U.S. market remains both a strength and a vulnerability. While the U.S. While the U.S. remains Mexico's largest trading partner, it is crucial that Mexico continues to diversify its markets to result in its long-term competitiveness.

Nearshoring remains a key strategy that Mexico must take advantage of to strengthen its industry. Despite the challenges of exchange rate volatility and tariff tensions, Mexico has demonstrated resilience in its foreign trade. The improvement in logistics infrastructure, record customs collection and foreign investment are a clear sign of Mexico's commitment to improving its commercial capabilities.

Mexico is in a privileged position to continue expanding its foreign trade. The diversification of products, markets and trading partners will be the key to consolidating its economic growth in the future, while strengthening the logistics infrastructure will allow the country to remain a key player in the global economy.

mantente al día con DICEX